Complex transactions, third-party vendor relationships and IT management all call for thorough TSAs.

By William Blandford, Managing Director at Blandford Associates and Member of the Board of M&A Standards

Why do so many divestitures fail to live up to their potential value? Transition Services Agreements (TSAs) often get overlooked or pushed off until far too late in the transaction. Yet a solid TSA certainly preserves deal value, especially in these three scenarios.

Transactions with Multiple “Layers” Such as a Carve-Out of a Carve-Out

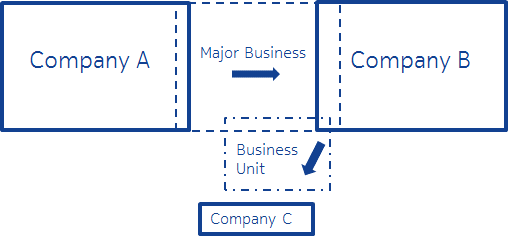

As companies begin to more aggressively incorporate divestitures into their growth strategies, complex M&A transactions with multiple “layers” will likely become more common. Consider one scenario that already happens on occasion: a carve-out of a carve-out. Company A carves out a major business and sells it to Company B. Then Company B quickly identifies and sells off one of the units of that business to Company C, before the TSA is fully executed between Companies A and B. In this case, the TSA to support the transition of the business unit from Company B to C is in place at the same time as the TSA between Companies A and B.

As companies begin to more aggressively incorporate divestitures into their growth strategies, complex M&A transactions with multiple “layers” will likely become more common. Consider one scenario that already happens on occasion: a carve-out of a carve-out. Company A carves out a major business and sells it to Company B. Then Company B quickly identifies and sells off one of the units of that business to Company C, before the TSA is fully executed between Companies A and B. In this case, the TSA to support the transition of the business unit from Company B to C is in place at the same time as the TSA between Companies A and B.

This situation leads to considerable overlaps among TSAs, even though there is no legal or contractual relationship between Company A and Company C. There will likely be times when Company C needs information, such as product history, but Company B has not yet obtained it yet. Meanwhile, Company C cannot go directly to Company A because these two companies have no legal relationship or obligation. Company C must hope that Company B has a provision in a TSA for obtaining product history. For simultaneous transactions like this to be successful, it is critical that the TSA be detailed and comprehensive. Read more.