Cash is King?

By Tony Enlow, Partner, Transaction Advisory Services at BDO and Board of M&A Standards Member

The adage “Cash is King” describes the importance of having enough cash in the business for short-term operations. But there’s a difference between having cash on paper and having it available to spend. Companies can have significant accounts receivable or inventory on the balance sheet but may not have enough cash to operate the business until the accounts receivable is collected or the inventory is processed and sold.

In the context of an acquisition, cash is often overlooked from a due diligence perspective. This makes sense in that the cash in the acquired company typically remains with the seller. A proper negotiated working capital to be delivered by the seller typically takes the place of cash on the balance sheet in an acquisition setting.

So, does cash matter at all in an acquisition? Yes, it does. The Buyer can perform various analyses related to cash to gain insight in the business, even though as an asset, cash is excluded from the deal. Here are three valuable analyses you can do as part of your due diligence procedures:

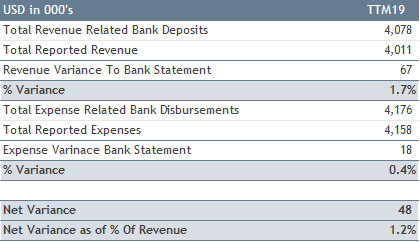

Proof of Cash

If the target is not audited, a proof of cash analysis can identify irregularities between cash receipts and revenue or cash disbursements and expenses. This analysis can be performed to validate that the revenue the target claims to have is valid. For revenue, you want to compare cash deposits each month for all bank accounts to the corresponding revenue. There are numerous reconciling items that need to be considered – including changes in accounts receivable or unbilled receivables as well as changes in deferred revenue, if any. Other reconciling items include cash transfers between bank accounts or cash deposits from non-revenue sources such as bank credit lines or litigation settlement monies. Depending on the number of bank accounts the target has, this analysis can take some time, so you want to allow additional time to reconcile each month. Similarly, for expenses, you want to compare total monthly disbursements for all bank accounts to the total operating expenses reported by the target. Again, there are numerous reconciling items for such non-cash expenses like depreciation and amortization, but also changes in accounts payable, accrued liabilities and prepaid expenses among others. Other reconciling items might include non-operating disbursements in the bank statements such as owner distributions or loan payments. This analysis will rarely reconcile 100%. The rule of thumb is that a variance of 3% or less in total is a tolerable variance that should give the Buyer some comfort in the numbers when combined with other diligence procedures. The table below details an example of the summary output of a proof of cash exercise.

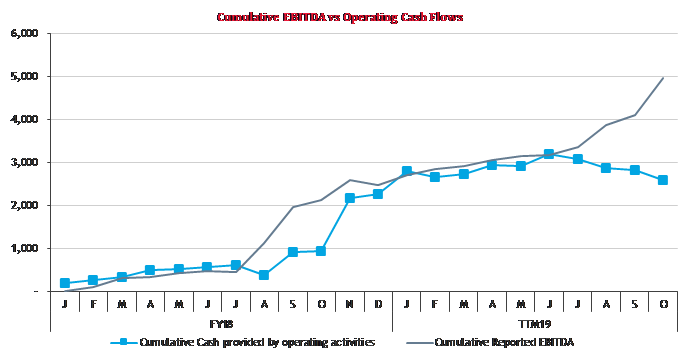

Cumulative EBITDA vs Cumulative Operating Cash Flows

This analysis begins with monthly income statements and monthly cash flow statements and displays the cumulative balance by month for each on the same chart. (See example below.) The purpose of this analysis is to see how well EBITDA tracks with cash flow from operations and if there are significant diversions between the two over time. If so, the Buyer should investigate. Diversions can be caused by significant changes in inventory or accounts receivable or other items included in cash flow from operations. This analysis is not a substitute for a thorough working capital or income statement analysis, but it can potentially help the Buyer focus on certain time periods where a divergence occurs. The chart below illustrates the outcome of this type of analysis.

In the above example, the divergence between cumulative EBITDA and cash flows from operations between these periods is primarily due to a significant increase in accounts receivable, consistent with the seasonality of the business. This analysis helps the Buyer understand the impact of seasonality on cash flows as well as when that cycle typically happens, allowing for a more thorough understanding of how the working capital should be analyzed.

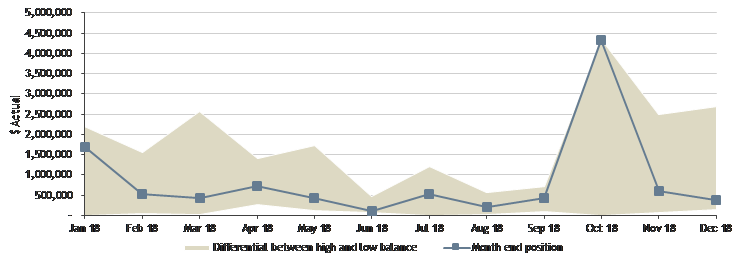

Intramonth Cash Balance Analysis

The third analysis involving cash is called the intramonth cash balance analysis. This analysis is generally performed monthly for the last twelve-month period and requires the target to provide the Buyer with the daily cash balances from each operating bank account. The analysis begins by charting the high and low balance for the month against the ending balance to give some insight as to when cash is tight and when the target is generally flush with cash and why. The answers may provide insights into seasonality or other issues that may need to be drilled down on further in the income statement or working capital analyses. The chart below details what a typical intramonth cash balance generates.

In the example above, October was the largest month in the Company’s history regarding billable man-hours worked during the month. Additional conversations with the target also revealed that the business was highly seasonal and was dependent on the turnaround schedules at major refineries. As a result, the working capital analysis focused on both seasonality and the turnaround schedules forecasted for the next six months.

Best practice is to include a cash analysis during due diligence, even though it usually is not one of the assets being acquired. The insight it provides can help your company maximize deal value by revealing other avenues of due diligence, and it can prepare you to effectively manage the newly acquired business. Don’t miss this chance to discover a wealth of information.

About Tony:

About Tony:

Tony Enlow has over 15 years of experience providing financial due diligence and transaction advisory services. He has worked on over 300 transactions ranging in size from $5 million to $40 billion and has assisted buyers and sellers that include private equity, public and private companies focused on transactional quality of earnings, cash flows and working capital. He has experience in a number of industries including agriculture companies, multi-location retail and restaurant, manufacturing, textiles, regulated and unregulated energy and energy related services, professional services, technology and many others. Let Tony prepare for your next M&A transaction at M&A Leadership Council's The Art of M&A Due Diligence in Scottsdale October 2019.